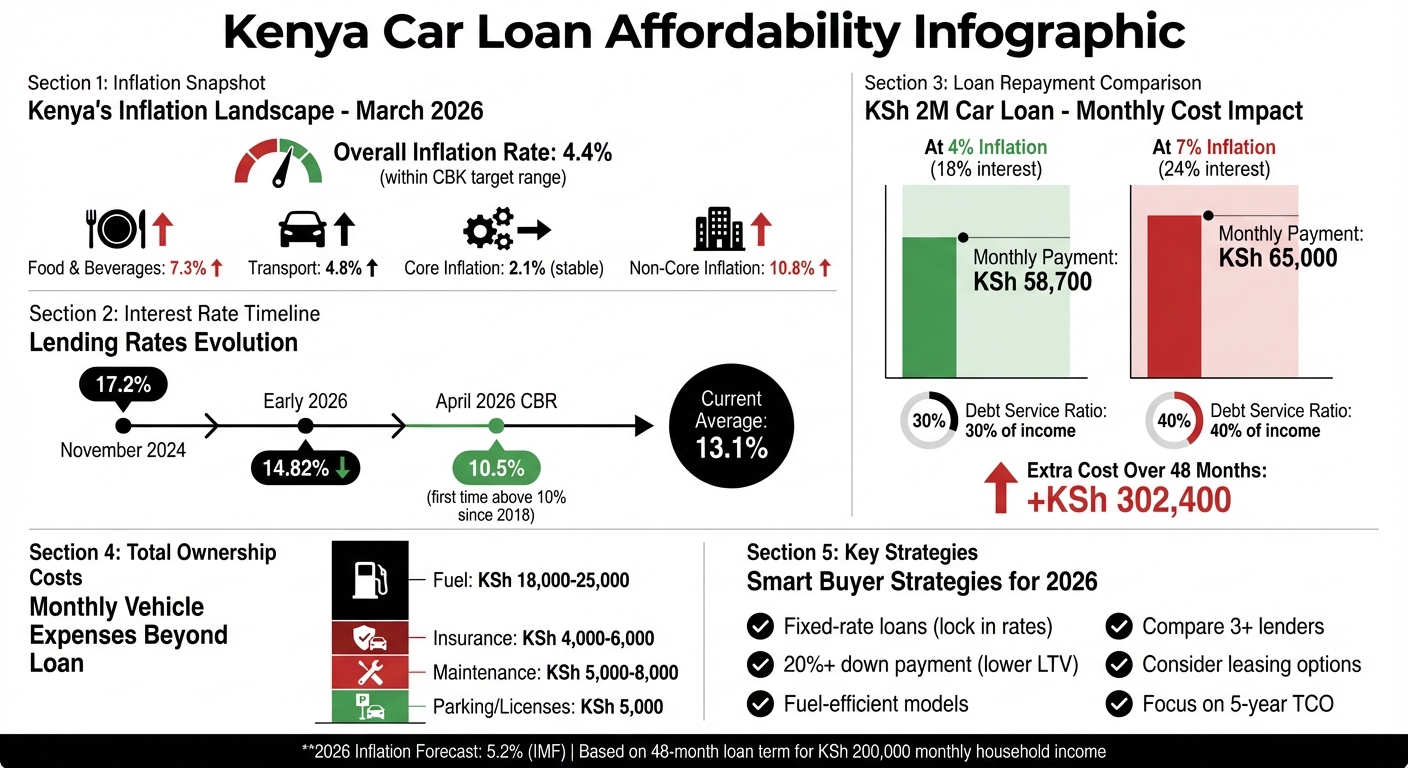

Kenya’s inflation rate of 4.4% in early 2026 has kept prices within the Central Bank’s target, but rising costs in food (7.3%) and transport (4.8%) are straining household budgets. Lower interest rates – now 14.82% for loans – have made car financing more accessible compared to 2024. However, a recent increase in the Central Bank Rate to 10.5% will likely lead to higher borrowing costs. For example, a KSh 2 million car loan at 18% interest translates to KSh 58,700 monthly payments, which can climb significantly with inflation or rate hikes.

Key takeaways:

- Stable inflation has eased lending conditions, but essentials like food and fuel remain costly.

- Vehicle financing costs are rising, with higher interest rates pushing monthly repayments.

- Buyers are opting for used cars, repossessed vehicles, or leasing to manage costs.

To navigate these challenges, consider fixed-rate loans, fuel-efficient models, or increasing down payments to lower borrowing needs. Planning around total ownership costs, not just loan repayments, is critical in 2026.

Kenya Car Loan Affordability: Inflation Impact on Monthly Repayments 2024-2026

How Car Financing Works in Kenya – Bob Wa Magari Visits Royal Max Motors | #SpaceYaMagari

sbb-itb-e5ed0ed

Inflation Trends in Kenya

Understanding how inflation changes month-to-month and over several years is key to grasping shifts in car loan costs.

Inflation Rates and Drivers (2025-2026)

In Kenya, inflation inched up to 4.4% in March 2026, slightly higher than February’s 4.3%, staying within the target range. However, the details reveal a split between stable and volatile price categories. Core inflation held steady at 2.1%, while non-core inflation rose from 10.1% in February to 10.8% in March.

Food and non-alcoholic beverages played a big role in driving inflation, with a 7.7% year-over-year increase. Certain vegetables saw steep price hikes – cabbages surged 33.8%, tomatoes rose 23.2%, and sukuma wiki was up 17.9% compared to March 2025. Other staples like beef (with bone) and fortified maize flour also saw increases of 9.6% and 6.9%, respectively. Transportation costs climbed 3.8% annually, while housing and utilities, including electricity, water, and gas, rose by 2.0%.

Electricity bills increased slightly, with households using more energy paying about KES 125 more. On the flip side, not all prices went up – gas prices for a 13 kg LPG cylinder dropped slightly, and cabbage prices per kilogram fell month-over-month from KES 74.33 to KES 71.52.

These short-term shifts are part of a broader trend of inflation cooling over the past two years.

Inflation Trends from 2024 to 2026

Looking at the bigger picture, inflation in Kenya has significantly eased over the last two years. It dropped from over 6% in early 2024 to about 4% by early 2026, signaling better macroeconomic stability. This improvement allowed the Central Bank of Kenya (CBK) to move from tight monetary policies to a more supportive approach, improving lending conditions.

"The core CPI basket accounts for 81.1% of the overall CPI, indicating that most consumer spending falls within relatively stable price categories." – Central Bank of Kenya (CBK)

The growing gap between core and non-core inflation highlights how seasonal factors, like food supply shocks, are straining household budgets. While manufactured goods and services remained stable, families felt the pinch from fluctuating food prices rather than widespread economic pressure. Energy costs, which were unpredictable in prior years, showed little movement in early 2026 – diesel prices rose just 0.1%, and LPG prices increased by only 0.4%.

This long-term stability, combined with seasonal food price spikes, has a direct impact on financing conditions for car buyers. These trends reveal the delicate balance between challenges and opportunities in Kenya’s car financing landscape.

How Inflation Affects Car Loan Costs

When inflation rises, the Central Bank of Kenya (CBK) responds by adjusting the Central Bank Rate (CBR), which has a direct impact on loan costs.

Central Bank Rate and Lending Costs

On April 9, 2026, the CBK raised the base lending rate from 9.5% to 10.5%, marking the first time the CBR had exceeded the double-digit threshold since January 2018. This move reflects tighter monetary policies aimed at controlling inflation. Commercial banks typically follow suit, increasing their lending rates within about 60 days of a CBR hike.

"Kenyans are bracing themselves for more expensive bank loans after the Central Bank of Kenya (CBK) increased its base lending rate from 9.5 per cent to 10.5 per cent." – Bernard Wafula

As a result, average lending rates at commercial banks rose from 12.4% in Q3 2022 to 13.1% by April 2026. For those financing a car, this translates to steeper interest costs, directly affecting monthly repayment terms.

Impact on Monthly Repayments

Even a small increase in the Annual Percentage Rate (APR) can push up your Equated Monthly Installment (EMI), limiting how much you can borrow. A Nairobi-based building supplies company experienced this in early 2025. Instead of purchasing a new Toyota Hilux, they chose more budget-friendly options: a certified pre-owned Isuzu D-Max and a repossessed Toyota Hiace. By comparing Total Cost of Ownership (TCO) and adjusting their EMIs, they managed to cut their monthly repayments by 18% over a 60-month loan term compared to financing two new vehicles.

Inflation doesn’t just affect loan repayments – it also increases the cost of imported vehicles. A weaker Kenyan shilling raises the Cost, Insurance, and Freight (CIF) value of imports, which in turn inflates taxes like import duty, excise, and VAT. This drives up the total amount you need to finance. Meanwhile, higher living expenses for essentials like fuel, food, and rent reduce disposable income, making it harder to manage the same monthly car loan payments within a tight budget.

Car Loan Affordability Analysis

Let’s dig deeper into how inflation affects household budgets, particularly when it comes to car loan repayments. With rising lending costs, the financial strain becomes more apparent.

Loan Repayment Examples Under Different Inflation Rates

To put things into perspective, let’s look at a KSh 2 million car loan with a 48-month term – a common choice for middle-income earners. When inflation is at 4%, lenders charge about 18% interest (on the lower end of the market). This translates to a monthly repayment of roughly KSh 58,700. Now, factor in operational expenses like:

- Fuel: KSh 18,000–25,000

- Insurance: KSh 4,000–6,000

- Maintenance: KSh 5,000–8,000

- Parking and licenses: KSh 5,000

For a household earning KSh 200,000 per month, this adds up to a debt service ratio of about 30% of disposable income.

But what happens when inflation climbs to 7%? Interest rates jump to 24%, pushing monthly repayments to approximately KSh 65,000. This increases the debt service ratio to over 40% of disposable income – a point where financial stability starts to wobble. Missing payments or skipping vital car maintenance becomes a real risk.

"When a family allocates 30 to 40 percent of their disposable income to loan repayments, fuel, and service, they lose the ability to invest that capital in yielding instruments." – Streamline Official

Now, consider the impact of just a KSh 6,300 monthly increase in repayments. Over 48 months, that adds up to an extra KSh 302,400. It’s a difference that could determine whether owning a car remains manageable or turns into a financial burden.

These numbers highlight the importance of careful financial planning, especially in an inflationary environment.

Inflation Forecasts and Buyer Strategies

2026 Inflation Forecasts

The International Monetary Fund (IMF) predicts that Kenya’s average inflation rate in 2026 will hover around 5.2%, staying comfortably within the target range of 2.5% to 7.5%. This stability has already influenced lending conditions, with average commercial lending rates dropping to 14.82% in early 2026, compared to 17.2% in November 2024.

"Inflation remained below the 5% midpoint of the target range, providing room to support economic activity through lower borrowing costs." – Dr. Kamau Thugge, Governor, Central Bank of Kenya

Adding to this favorable environment, the Risk-Based Credit Pricing Model, launched in March 2026, has introduced more predictable financing options. This is particularly good news for car buyers, as it creates opportunities to secure better rates despite inflationary pressures. These developments highlight the importance of strategic financial planning for anyone looking to make significant purchases.

Cost Management Strategies for Buyers

With inflation projected to remain steady, buyers can fine-tune their financial strategies to make the most of the current conditions. For instance, opting for fixed-rate loans ensures stability by protecting against potential interest rate increases down the line.

For those looking to avoid the upfront costs associated with traditional ownership, vehicle leasing platforms like AUTO24.co.ke provide a flexible option. Leasing can help manage monthly cash flow, especially when high-interest financing feels burdensome. Alternatively, for buyers committed to purchasing, choosing budget-friendly, fuel-efficient models – as recommended on AutoMag.co.ke – can help offset rising costs in areas like food and utilities. Another smart move is increasing your down payment to 20% or more, which not only lowers the loan-to-value ratio but can also lead to reduced interest rates and more manageable monthly payments.

Conclusion

Kenya’s 2026 car-buying trends are shaped by a mix of stabilized inflation and evolving buyer strategies. While headline inflation has steadied at 4.4% and lending rates have eased to 14.82%, food inflation remains high at 7.3%, straining household budgets. These economic dynamics are driving shifts in how Kenyans approach vehicle purchases.

As discussed, many buyers are turning to late-model used cars and repossessed vehicles to cut upfront costs. Others are prioritizing vehicles like the Toyota Hilux, Isuzu D-Max, and Toyota Fielder, known for their strong resale value, to safeguard their investment against depreciation. This shift reflects a broader effort to adapt to financial pressures.

Rising financing costs further complicate budgets, with even small payment increases having the potential to disrupt household finances. To navigate these challenges, smart buyers are comparing at least three lenders – including SACCOs, which often provide better rates – and securing favorable foreign exchange terms for imports to counter currency fluctuations.

Ultimately, affordability in 2026 depends on meticulous financial planning. Whether you opt for a fixed-rate loan, explore leasing options through platforms like AUTO24.co.ke, or choose a fuel-efficient vehicle, the focus should be on the total five-year ownership cost – not just the monthly payment. Careful planning remains the key to overcoming inflationary pressures and making sound financial decisions.

FAQs

Should I choose a fixed-rate or variable-rate car loan in 2026?

In Kenya, deciding between a fixed-rate or variable-rate car loan in 2026 largely hinges on inflation and the state of the economy. With inflation hitting a six-month low of 4.4% in January 2026, fixed-rate loans provide the advantage of consistent payments by locking in your interest rate. On the other hand, if interest rates stay steady or drop further, a variable-rate loan might help you save on costs. When making your choice, think about your financial situation, how much risk you’re comfortable with, and the range of options available from lenders.

What’s the safest debt-to-income level for a car loan in Kenya?

A debt-to-income ratio of 43% or lower is typically seen as the safest benchmark for car loans in Kenya. Keeping your ratio below this level not only boosts your chances of getting approved but can also lead to more favorable loan terms.

How do shilling exchange rates affect the final price of imported cars?

When the shilling depreciates, exchange rates directly affect the final cost of imported cars by driving up the landed cost. This increase cascades into higher import duties, taxes, and overall vehicle prices. As a result, many consumers in Kenya find imported cars increasingly out of reach.

Related Blog Posts

- Car prices in Nairobi 2025

- Why Car Prices in Kenya Are Changing in 2025

- New vs Used Cars in Kenya: What You’ll Pay in 2025

- 5 Economic Trends Shaping Kenya’s Car Market

{kind=link}