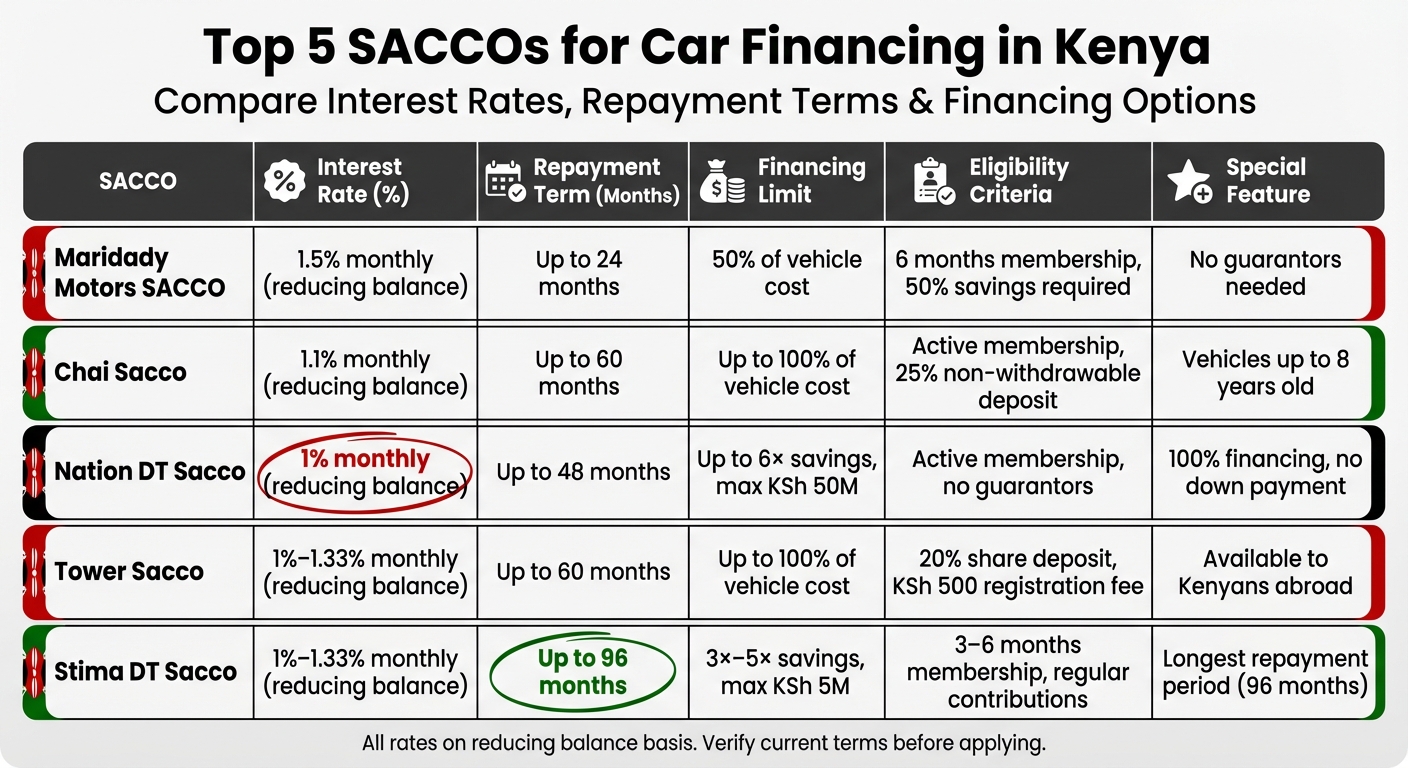

SACCOs (Savings and Credit Cooperative Organizations) offer a cost-effective alternative to bank loans for car financing in Kenya. With lower interest rates, flexible repayment terms, and member-focused benefits, they’re a preferred option for many. Here’s a quick rundown of the top five SACCOs for car loans:

- Maridady Motors SACCO: Ideal for informal sector workers with a 50/50 savings and financing model. Interest is 1.5% monthly (reducing balance) with up to 24 months for repayment.

- Chai Sacco: Offers up to 100% financing for vehicles under 8 years old. Interest is 1.1% monthly (reducing balance) with a 60-month repayment term.

- Nation DT Sacco: Provides 100% financing with no down payment. Interest starts at 1% monthly (reducing balance) with up to 48 months for repayment.

- Tower Sacco: Covers up to 100% of the vehicle cost. Requires a 20% share deposit and offers repayment terms of up to 60 months.

- Stima DT Sacco: Features various loan products with interest rates starting at 1% monthly (reducing balance) and repayment terms of up to 96 months.

Quick Comparison

| SACCO | Interest Rate | Repayment Term | Financing Limit | Eligibility |

|---|---|---|---|---|

| Maridady Motors | 1.5% monthly | Up to 24 months | 50% of vehicle cost | 6 months membership, 50% savings |

| Chai Sacco | 1.1% monthly | Up to 60 months | Up to 100% of vehicle cost | Active membership, 25% deposit |

| Nation DT Sacco | 1% monthly | Up to 48 months | Up to 6× savings, max KSh 50M | Active membership, no guarantors |

| Tower Sacco | 1%–1.33% monthly | Up to 60 months | Up to 100% of vehicle cost | 20% share deposit, membership fee |

| Stima DT Sacco | 1%–1.33% monthly | Up to 96 months | 3×–5× savings, max KSh 5M | 3–6 months membership, savings |

Each SACCO has unique benefits, so choose one based on your savings, repayment capacity, and vehicle needs. Always verify current terms and conditions before applying.

Top 5 SACCOs for Car Financing in Kenya: Interest Rates and Terms Comparison

A few Saccos in Kenya that offer car financing without collateral

sbb-itb-e5ed0ed

1. Maridady Motors SACCO

Maridady Motors SACCO provides a 50/50 financing model, designed to help workers in Kenya’s informal sector – like taxi drivers, boda boda riders, and mechanics – purchase vehicles. Once you save half the vehicle’s cost, the SACCO funds the remaining half. No guarantors are needed if you meet the savings requirement.

"The client will save with us up to 50 per cent of the cost of the car or machinery and we finance the remaining 50 per cent through the Maridady Sacco", explains Eric Mwangi, CEO of Maridady.

Interest Rate

The "My Ride Account" car financing product comes with an interest rate of 1.5% per month, calculated on a reducing balance. Payments can be made in smaller, more manageable amounts throughout the month.

Maximum Repayment Period

Borrowers have up to 24 months (2 years) to repay their car loans. This flexible repayment period is tailored to accommodate the often-variable income patterns of informal sector workers.

Eligibility Requirements

To qualify for financing, you need to meet the following criteria:

- Be an active SACCO member for at least 6 months.

- Pay a one-time registration fee of KSh 5,000.

- Save 50% of the vehicle’s cost in your "My Ride Account."

For example, taxi drivers might save KSh 2,000 daily to reach a KSh 350,000 goal, while boda boda riders could save KSh 300 daily for a motorbike. Unlike traditional lenders, Maridady Motors SACCO does not require bank statements or CRB checks, making it accessible to those with limited formal financial records.

2. Chai Sacco

Chai Sacco provides car financing through its Asset Finance product, catering to both new and used vehicles, as long as the vehicle is no older than 8 years.

Interest Rate and Repayment Terms

Car loans from Chai Sacco come with an interest rate of 1.1% per month on a reducing balance, with repayment periods of up to 60 months.

Financing Percentage and Conditions

Chai Sacco offers financing for up to 100% of the vehicle’s purchase price, provided certain conditions are met. Borrowers need to make a non-withdrawable deposit equal to 25% of the vehicle’s value, and the car must meet the age limit of 8 years from the date of manufacture.

Eligibility and Additional Costs

To qualify, you must be an active member of the SACCO. The loan is secured using the vehicle’s logbook or a title deed. Borrowers should also budget for extra expenses, including car tracking, comprehensive insurance, and valuation fees.

3. Nation DT Sacco

Nation DT Sacco offers an appealing option for car buyers by providing 100% motor vehicle financing, requiring no down payment. Established in 1975 for employees of Nation Media Group, the SACCO expanded its membership to the public in 2010 and operates under a SASRA license for deposit-taking services.

Interest Rate and Repayment Terms

Their car loans feature interest rates starting at 1% per month on a reducing balance, with repayment terms extending up to 48 months.

Financing Percentage and Loan Limits

Nation DT Sacco provides full vehicle financing, but the loan amount is tied to your savings. Members can borrow up to six times their savings, with a maximum loan cap of KSh 50,000,000. For instance, if you save KSh 500,000, you could qualify for a loan of up to KSh 3,000,000.

Eligibility Requirements

To access car financing, you must be an active member of Nation DT Sacco. The SACCO simplifies the process by accepting collateral instead of requiring guarantors. Membership registration is convenient through their mobile app, available on both Google Play and the App Store. Additionally, their online loan calculator helps estimate monthly repayments based on a reducing balance. This combination of full financing and flexible terms makes Nation DT Sacco a standout choice in Kenya’s car financing sector.

4. Tower Sacco

Tower Sacco provides Asset Finance loans specifically designed for purchasing motor vehicles. Their services are available to a wide range of members, including business owners, salaried employees from government, TSC, and private sectors, as well as Kenyans living abroad. Here’s what you need to know about their car financing options:

Maximum Repayment Period

Borrowers can benefit from a maximum repayment period of 5 years (60 months), making it easier to manage payments over an extended timeline.

Financing Percentage and Deposit Requirements

Tower Sacco offers financing for up to 100% of the vehicle’s cost, but members must contribute a minimum share deposit equivalent to 20% of the asset’s value. For example, if the car costs KSh 1,500,000, you’ll need to provide a minimum share deposit of KSh 300,000.

Eligibility Requirements

To apply, you must be a registered member. Here’s what that entails:

- Pay a KSh 500 registration fee for premium individual membership.

- Maintain a minimum share capital of KSh 2,000.

- If self-employed, your business must have been operational for at least 6 months.

The loan is secured by your deposits, the vehicle itself, and qualified guarantors. Additionally, comprehensive insurance coverage for the vehicle is mandatory.

5. Stima DT Sacco

Stima DT Sacco brings a range of flexible car financing options, leveraging over 50 years of experience. They offer several loan products designed to meet different needs, including Normal, Super, Vuka, and Premium Loans. The loan amounts are based on a multiplier of your alpha deposits (non-withdrawable savings).

Interest Rate (Per Month Reducing Balance)

The interest rates for Stima DT Sacco loans depend on the product you choose:

- Normal Loan: 12% per annum (approximately 1% per month on a reducing balance)

- Super Loan: 14% per annum (about 1.17% per month)

- Vuka Loan: 16% per annum (roughly 1.33% per month)

- Premium Loan: 13% per annum (around 1.08% per month), with a repayment period of up to 96 months.

Maximum Repayment Period (Months)

Repayment terms vary by loan type:

- Normal Loan: Up to 60 months

- Vuka Loan: Up to 72 months

- Premium Loan: Up to 96 months

Financing Percentage

The borrowing limits are tied to your alpha deposits:

- Normal and Super Loans: Up to four times your alpha deposits

- Premium Loan: Up to five times your alpha deposits

- Vuka Loan: Maximum limit of KSh 5 million

Eligibility Requirements

Eligibility depends on membership duration and contributions:

- Individual Members: Minimum of 3 months’ membership

- Corporate Members: Minimum of 6 months’ membership

Applicants must also meet share capital requirements and maintain regular monthly contributions. For example, the Vuka Loan requires a minimum monthly contribution of KSh 7,500. Applications can be submitted via the Stima Sacco mobile app (M-Pawa), the online member portal (Msasa), or in person at a branch. Required documents include your national ID, membership number, and recent payslips for verification.

SACCO Comparison Table

When evaluating SACCOs, it’s helpful to consider factors like interest rates, repayment terms, financing limits, and membership requirements. Typically, SACCOs offer more affordable rates compared to commercial banks (13%–18.5% annually) and non-bank lenders (which can go as high as 36% annually).

Here’s a breakdown of the key terms for Stima DT Sacco:

| SACCO Name | Interest Rate (Per Annum) | Repayment Term | Financing Limit | Minimum Membership Duration |

|---|---|---|---|---|

| Stima DT Sacco | 12.75% (Reducing Balance) | Up to 36 months | Up to 3× savings | 3 months (Individual) / 6 months (Corporate) |

What makes Stima DT Sacco appealing is its competitive interest rate of 12.75% per annum, calculated on a reducing balance. Additionally, the membership requirement is relatively flexible, allowing individuals to qualify for financing after just three months of membership. The loan eligibility is tied to your savings, meaning the more you save, the larger the loan amount you can access. This structure encourages financial discipline while offering accessible credit options.

Conclusion

Exploring financing options through SACCOs highlights a range of accessible and budget-friendly ways to own a car. SACCO car loans offer an appealing alternative in Kenya, especially when compared to commercial banks, which typically charge annual interest rates between 14% and 21%, or non-bank lenders, whose rates can soar as high as 36%. With rates starting as low as 12% on a reducing balance basis, SACCOs like Stima present terms that could lead to significant savings over time.

The process, however, requires a clear understanding of each SACCO’s requirements. This approach not only promotes better financial habits but also allows individuals to purchase vehicles without needing a hefty initial payment.

Make sure to verify how the reducing balance method is applied and be on the lookout for hidden costs, such as processing fees, insurance premiums, or negotiation charges. Additionally, check whether the SACCO uses the vehicle’s logbook as collateral or requires personal guarantors, as these factors can affect your eligibility and borrowing flexibility.

Since interest rates and terms may shift due to Central Bank of Kenya regulations or internal SACCO adjustments, it’s always wise to consult with a credit officer for the most up-to-date information. Don’t forget to consider the full cost of ownership, including insurance, fuel, and maintenance, when comparing financing options.

FAQs

How does a reducing-balance car loan work in a SACCO?

When you take out a reducing-balance car loan through a SACCO, the interest is calculated on the remaining loan balance rather than the original amount. Since the balance decreases with every repayment, your interest payments also shrink over time. For instance, with a monthly interest rate of 1%, the interest is charged only on the outstanding balance. This approach helps lower the total interest you pay as you continue repaying the loan.

What extra fees should I budget for besides the loan interest?

When taking out a loan, it’s important to account for more than just the interest rate. Lenders often include additional costs like processing fees, insurance premiums, legal fees, and administrative charges. These expenses can vary widely depending on the lender, so it’s essential to go over the terms thoroughly before signing anything.

Can I get a SACCO car loan without guarantors or a CRB check?

Some SACCOs in Kenya offer car loans without the need for guarantors or CRB checks. For instance, Maridady SACCO provides these loans, emphasizing that they skip CRB checks and guarantor requirements. However, it’s always a good idea to verify the specific terms and conditions directly with the SACCO before proceeding.

Related Blog Posts

- Car Loan Eligibility in Kenya: Key Factors

- Car insurance costs in Kenya

- How to Get Car Financing in Kenya: Tips for First-Time Buyers

- How to Finance a Car in Kenya: What You Should Know

{kind=link}